Part 2: The Money Management System That Actually Works

How We Track Every Dollar Without Losing Our Minds

This is Part 2 of our ADHD money management series. Start with [Part 1: From Coffee Shock to Financial System] to understand the revelation that started it all.

Remember that coffee shop moment from Part 1? When I realized my ADHD brain needed a completely different approach to money management?

Six months later, I'm here with an update: the system works. Not just on paper, but in real life, with real challenges, real impulse purchases, and real ADHD brain fog.

Today I'm sharing exactly what we do now – the apps, the spreadsheets, the monthly rituals that form our three-pillar foundation.

The Current Setup: Three Pillars That Changed Everything

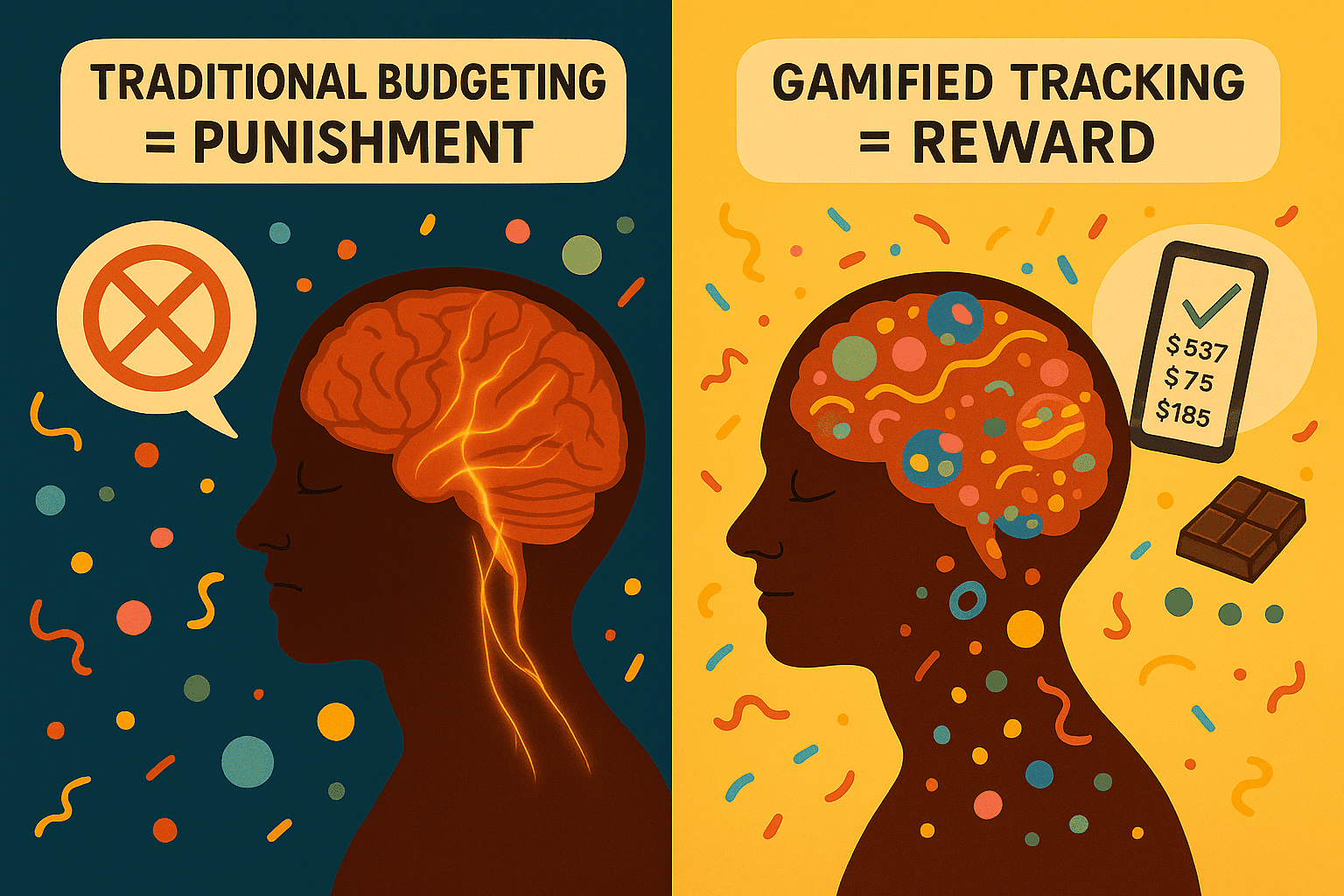

1. The Tracking App Revolution

What we use now: SpendTogether (switched from MoneyLover)

Why it works: Better couple integration and simpler interface

But here's the thing – the app isn't the magic. The magic is in what I call "gamified logging."

Every time I enter a transaction, I give myself a tiny reward. Sometimes it's a piece of chocolate. Sometimes it's checking off a satisfying checkbox. Sometimes it's just the mental "good job" that my ADHD brain craves.

The golden rule: Track EVERYTHING. Online purchases, cash transactions, that random coffee. The complete picture matters more than perfection.

Alternative apps to consider: Splitwise, Honeydue, YNAB, or even a simple shared note app – find what fits your brain. You can even drop simple notes to GPT later to help with calculations.

The Art of ADHD-Friendly Categorization

Here's something we've learned through trial and error: categories make or break the system for ADHD brains.

Too few categories = everything goes into "miscellaneous" and you lose insights

Too many categories = decision paralysis every time you log an expense

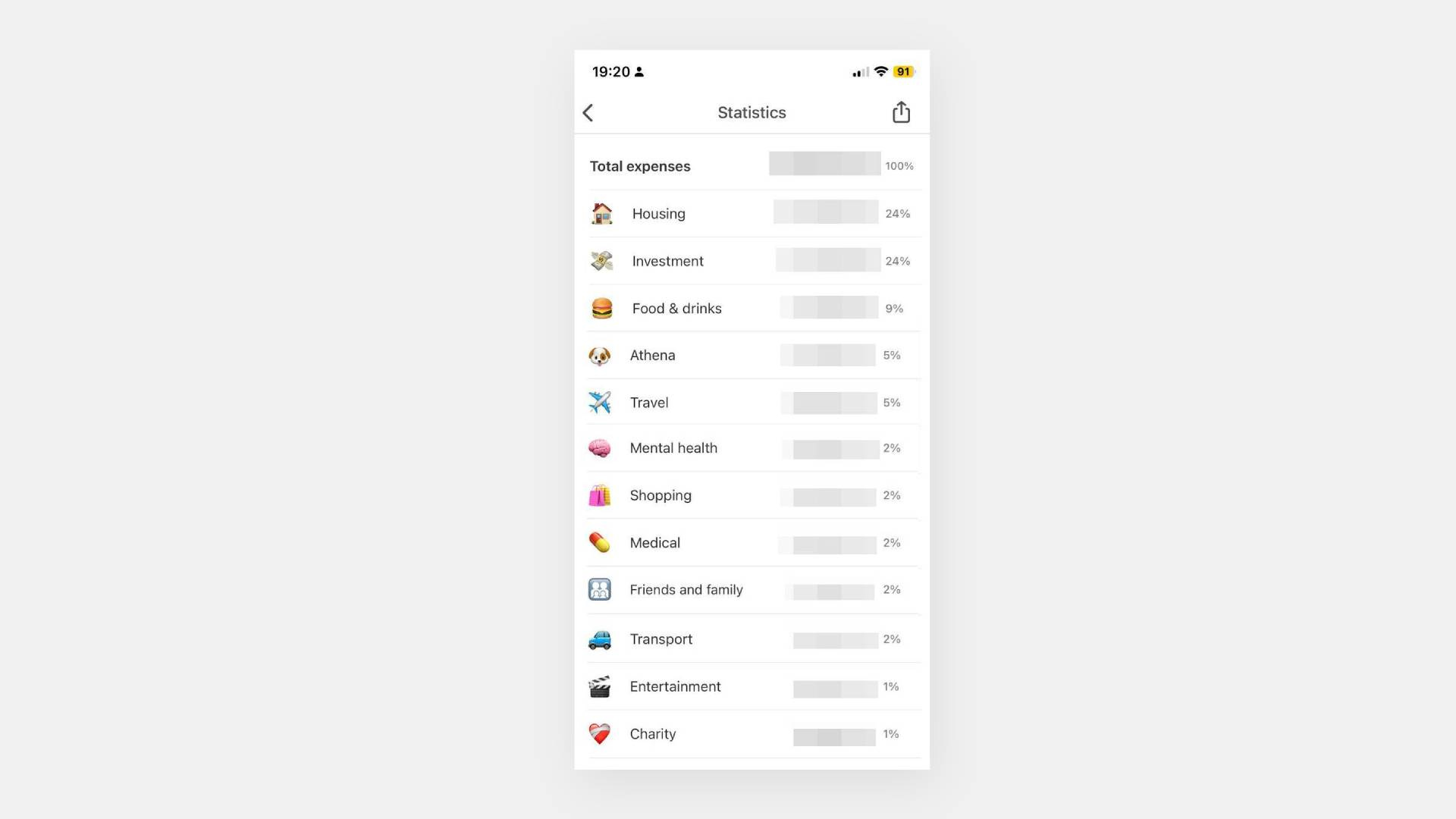

Our current setup has evolved over months of experimentation. Looking at our breakdown, you can see we balance major life areas with ADHD-specific needs:

The Big Three (our foundation):

Housing (24%) - rent, utilities, home essentials

Investment (24%) - our future selves thank us

Food & drinks (9%) - fuel for the ADHD brain

Life Categories (the middle ground):

Travel (5%) - because experiences matter

Athena (5%) - our dog's expenses (yes, pets get their own category)

Transport (2%) - getting around town

ADHD-Specific Categories (the game-changers):

Mental health (2%) - therapy, apps, brain care investments

Medical (2%) - separate from mental health for tracking

Shopping (2%) - impulse purchases get their own space

Entertainment (1%) - dopamine activities

Charity (1%) - giving back feels good

The Personal Touch:

Friends and family (2%) - social connections are investments too

Key insight: Your categories should reflect your actual life and values, not some generic budget template. Notice how we don't have traditional categories like "clothing" or "utilities" - instead, we have "Shopping" and everything home-related goes under "Housing."

Pro tip: Start with broader categories and split them as patterns emerge. We didn't start with "Mental health" and "Medical" as separate categories – they evolved when we realized we were making very different types of health investments.

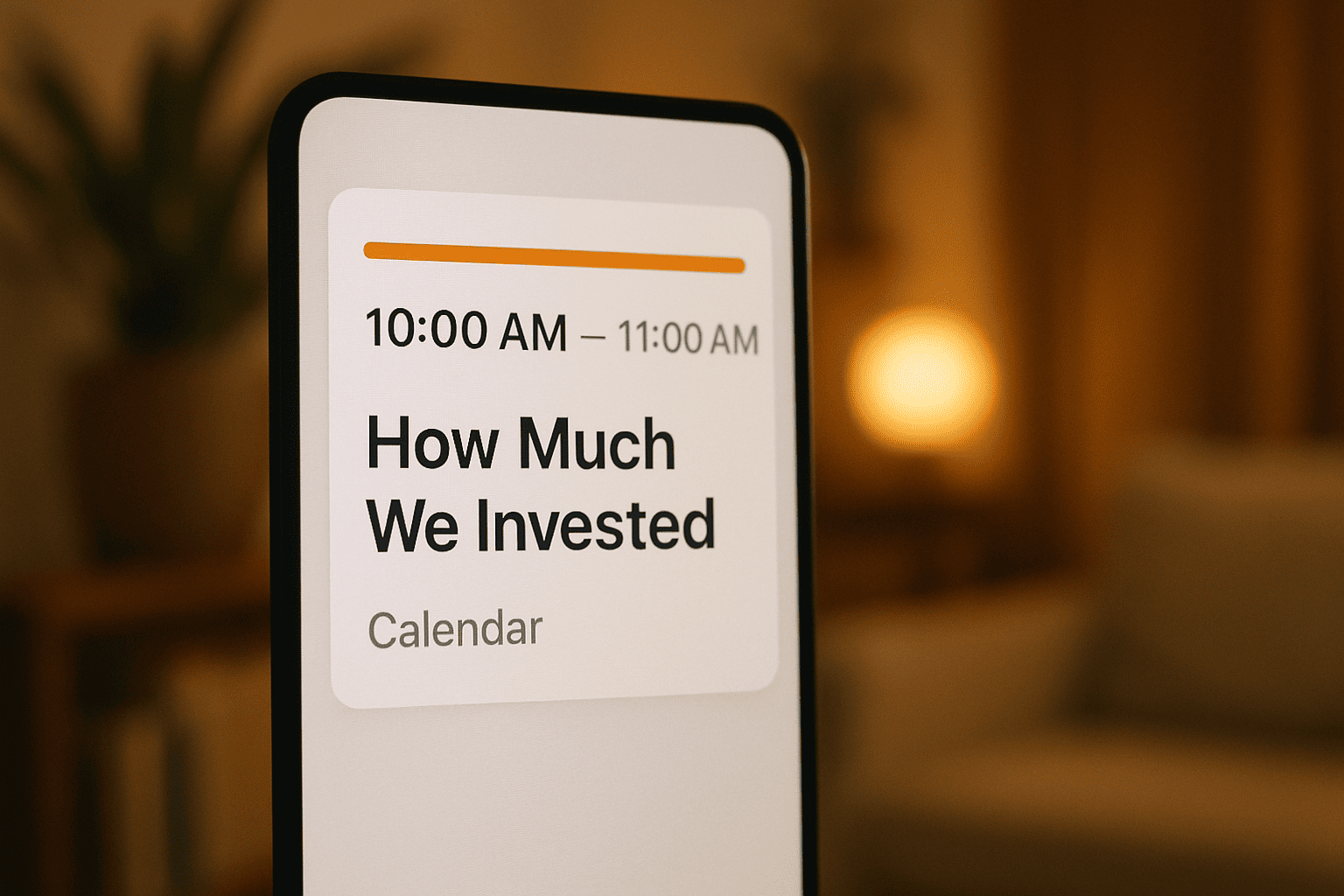

2. The Monthly Investment Meeting

Calendar event: "How Much We Invested" (last week of each month)

Duration: 30-45 minutes

Mindset shift: We focus on investments, not expenses.

This single word change – from "spending review" to "investment review" – transformed our entire relationship with money. Instead of feeling guilty about expenses, we celebrate what we put toward our future.

Our agenda:

Review tracking app totals

Update the spreadsheet

Celebrate investment wins

Plan next month's priorities

Address any tracking gaps

3. The Magic Spreadsheet

I've created a template that actually works for ADHD brains: [Google Sheets Template Link]

Key features:

Two tabs: Singles and Couples versions

The "Invested" column (this is the magic)

Here's our hack: We add our automatic investment transfers as "expenses" in the tracking app (because the money leaves our account), then subtract them in the spreadsheet. This gives us the real picture of our lifestyle spending while keeping investments visible.

Putting It All Together: The Three-Pillar Foundation

These three pillars work together to create what I call "sustainable financial awareness" for ADHD brains:

The tracking app gives us the daily dopamine hits we need to stay consistent

The monthly investment meetings reframe our relationship with money from shame to celebration

The magic spreadsheet provides the big picture without overwhelming detail

But here's what I've learned over these six months: the tools are just the beginning. The real transformation happens when you understand the psychology behind why this works for ADHD brains - and why traditional budgeting advice fails us so spectacularly.

The difference between a system that works and one that gets abandoned after two weeks isn't in the apps or spreadsheets. It's in understanding how to work with your ADHD brain instead of against it.

That's where the real magic happens - and it's what we'll dive into next.

Coming up in Part 3: The psychology that makes it stick, why gamification works for ADHD, and the mindset shifts that transform money management from a chore into something you actually want to do.

Ready to get started? [Copy the spreadsheet template] and pick an app that feels right for your brain. The most important step is just beginning.

Missed Part 1? [Start here with the coffee shop story] that sparked this whole system.

Interesting.

I track everything I spend in a spreadsheet, with categories totals etc.

It's interesting to see where my money goes but my financial situation has only gotten worse!

It was definitely helpful in the beginning as I could see what I'm spending and then cut out things and cancel out goings etc.

But now it's settled down, it's not as helpful in that regard.

To be honest, I'm just obsessed with tracking and measuring stuff (calories, steps, sleep, exercise, food portions, spending, weight, headaches, etc).

I think I do it because otherwise the chaos would be too much. Imagine not knowing how many grams of protein are in the food you've cooked or how many steps you did yesterday?! 😱😂

My money problems come down to spending more than I earn (because I procrastinate instead of work) and I can't seem to change that.

Sorry for the rambling comment!